e-INVOICE, e-ARCHIVE AND e-BOOK TRANSITION PACKAGES GIFTS CREDITS

WHAT IS e-BOOK?

WHAT IS e-BOOK?

The entirety of information required to be kept in book according to the Tax Procedure Law and/or Turkish Commercial Law independent of form provisions.

WHO IS UNDER THE COPE OF e-BOOK

Companies using e-Book and e-Invoice are legally obliged to use but all voluntary companies can use e-Book. This way they will be exempt from having their books certified, printed and having to save them for 10 years.

WHAT IS e-ARCHIVE?

e-Archive is the practice which allows natural and juridical persons who are not obligated to issue e-invoive to issue bills in electronic platform in accordance with the General Communique on the Tax Procedural Code (Serial No. 433)

WHO IS UNDER THE COPE OF e-ARCHIVE?

Taxpayers who sell goods or/and provide service online, and whose gross sales revenue on the income statement of 2014 is above 5 million TL, are obligated to use e-Archive practise by 1.1.2016

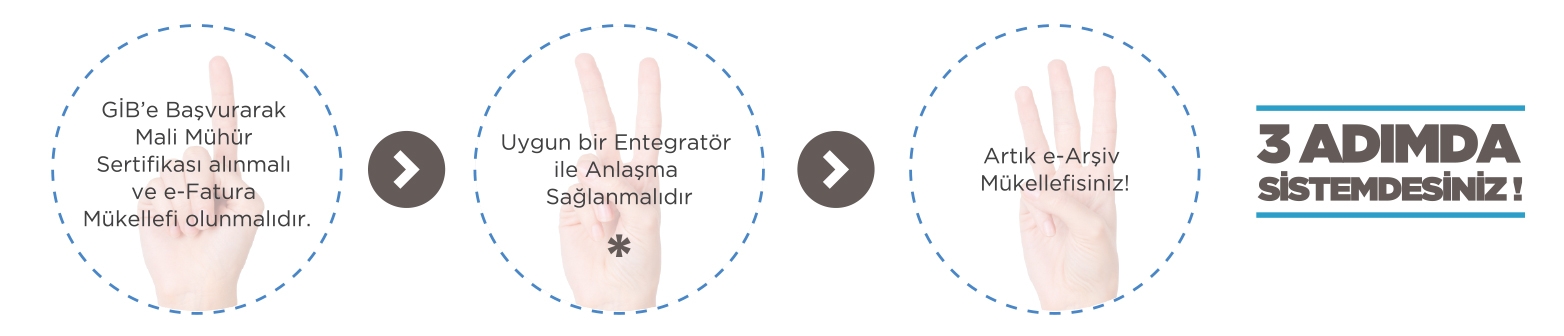

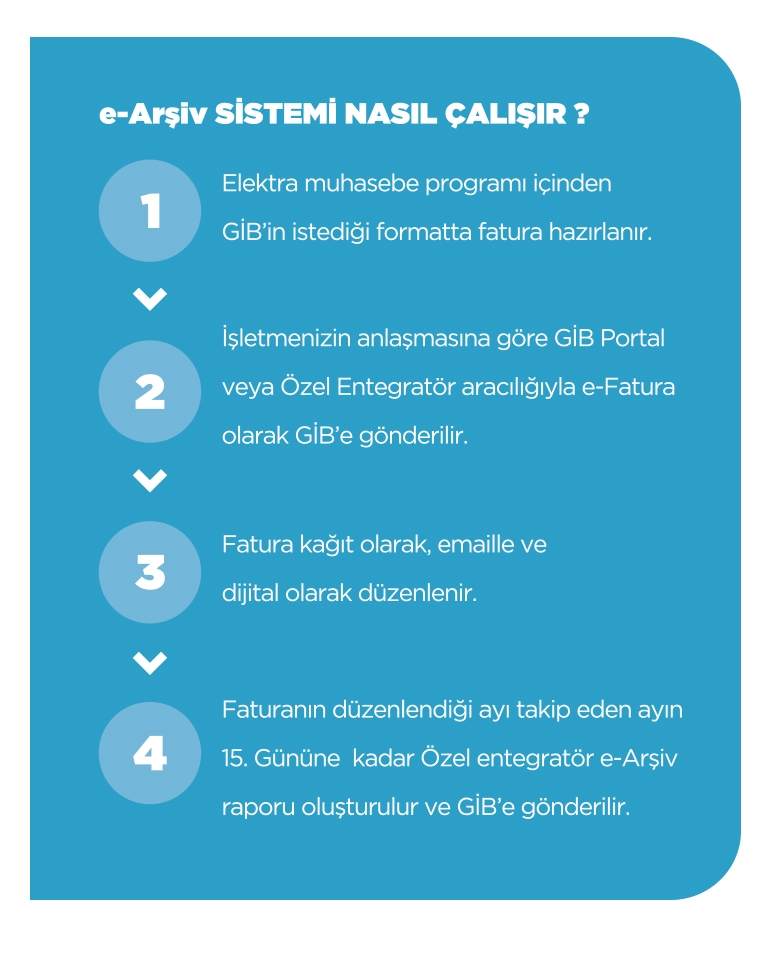

HOW YOU CAN BECOME A PART OF THE e-ARCHIVE SYSTEM?